A token itself may not be a security, but the method of its sale and usage could classify it as such.

The purest and sincerest response to the whole question of whether cryptocurrencies will be seen as securities by government agencies or not is: who cares. Because crypto’s intrinsic values are precisely censorship resistance and decentralization, its pillars make it impervious to governmental overreach. However, this ethos shouldn't blind us to the impact of traditional legal frameworks on the crypto sphere, particularly as rulings might influence the value and liquidity of various projects.

As @BawdyAnarchist_, a prominent voice in the Monero community, wisely stated: "If you want to understand the world better learn to containerize your thinking. I'm an anarchist but I can think inside legal paradigms. I want free markets but I can think inside the Keynesian paradigm." That’s exactly what motivates me to try to understand this better.

Let me preface by stating that I'm not a legal expert. The purpose of this article is to simplify the complex ruling on Ripple Labs' XRP token to enhance my understanding and hopefully yours. More importantly, as a cryptocurrency holder, I'm interested in how this might affect the status of the cryptos I hold.

Let’s start by asking what is a security? Securities typically fall into debt securities (like banknotes, bonds, and debentures), equity securities (such as common stocks), and derivatives (options, futures). These instruments entitle the holder to ownership rights in the issuing company, often with the potential for investment returns.

Recently, the U.S. Federal Court delivered a landmark judgment on the status of Ripple Labs' XRP token, creating a seismic shift in the cryptocurrency landscape. The court declared that XRP does not constitute a security, but noted that Ripple Labs' XRP sales to institutional customers amounted to an illegal securities offering.

This ruling could potentially reshape the regulatory approach towards platforms like Binance, Coinbase, and Kraken, already facing regulatory scrutiny from the SEC for the sale of unregistered securities.

The SEC's lawsuit against Ripple Labs centered on the classification of the XRP token as a security and whether its sale represented an unregistered securities offering. The court, however, dismissed the SEC's claims, ruling that XRP does not meet the Howey Test's requirements for an investment contract, causing a ~100% surge in XRP's price.

Interestingly, the court differentiated between XRP distributions, labeling the token's sale to institutional customers as a securities offering, but excluding algorithmic sales on exchanges to anonymous buyers and usage as compensation for employees and other parties from this classification.

The Nuance: Institutional Sales as Securities

While the XRP token ruling was celebrated in many quarters, it wasn't an outright win for Ripple Labs. Yes, the judge decided that XRP tokens are not securities. Despite XRP's classification as a non-security, the $728.9 million XRP sales to institutional investors were deemed an unregistered securities offering. The court refuted Ripple Labs' claim of XRP being a currency or utility token, noting that many investors agreed to hold their XRP for a specified period, signifying their speculative nature. Furthermore, contracts stated that buyers purchased XRP for reselling or distribution purposes

The judgment heralds a critical distinction in cryptocurrency regulation, positing that while a token itself might not be a security, its use and sales methods can categorize it as such.

But how does this apply to other cryptocurrencies? With coins like Monero and Litecoin, which have always employed a proof-of-work distribution method, the answer is straightforward. They are clearly so Bitcoin-like that whatever applies to Bitcoin, applies to them (ie. they are obviously commodities). However, what about other, more intricate examples? One example is Ethereum for instance, which had a big premine yet the CFTC nevertheless called it a commodity and the SEC refused to call it a security in its recent list of projects it named as securities.

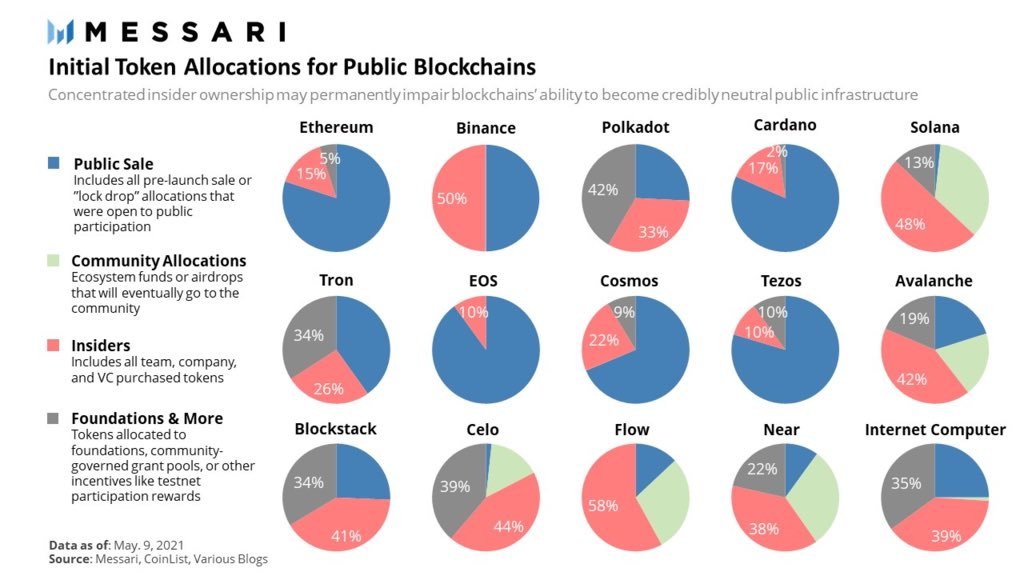

I remember that around 2014, with the first altcoin craze (a flurry of Litecoin clones), a cryptocurrency launch sans a 100% PoW distribution was often seen as a scam. Over time, this perception has shifted, and a properly disclosed premine is no longer viewed negatively. Take a look at how some of the currently biggest mcap altcoins have distributed their tokens:

Let's take Ethereum as an example. Even though SEC hesitates to call it a security, and even though most of the sale of the premine was public, Ethereum Foundation still did sell investment contracts, as they sold tokens directly to investors, and made promises of developing the platform, with the expectation of profit. The SEC is tactically refusing to call it a security, ostensibly to avoid controversy with the CFTC calling ETH a commodity, however, given the above, it is likely ETH would be found to have sold investment contracts in a trial.

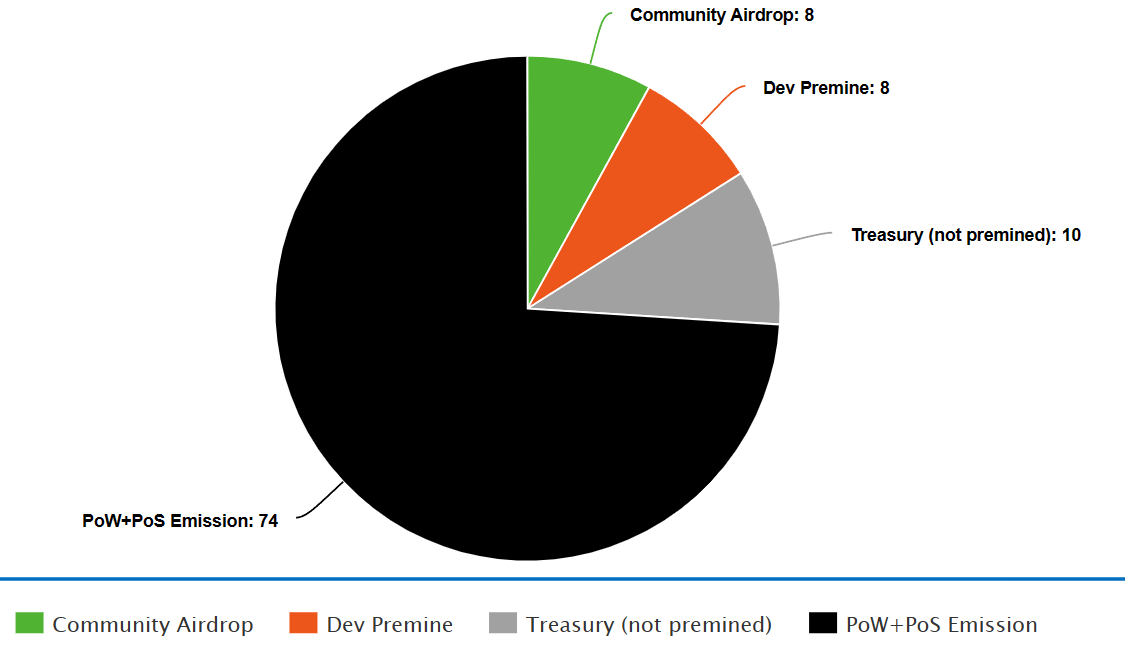

Let’s take Decred as another example that could be interesting to analyze for this purpose, a project I once labeled as a "Peer-to-peer Electronic Corporation", a characterization that makes it especially relevant here. In 2016, Decred conducted a premine where 840k coins were distributed to the developers, and an equal amount was allocated via a community airdrop. The purpose was to establish a pool of initial stakers, who could then serve as trusted validators. The developers were also permitted to buy coins at a fixed rate, accounting for less than 2% of the total distribution. The premine was followed by a PoW mining process or staking, with the tokens sold on exchanges.

However, the central issue is whether such a method of premine distribution could be viewed as a securities offering. Based on the recent ruling, the compensation to developers wouldn't qualify as a security offering. The court held that it isn't the token itself, but its function, sales method, and usage that deem it a security.

So, does Decred meet these conditions? The initial distribution was crucial for network security and community establishment.

Howie Test Applied, Taking Decred as an Example and Keeping XRP Ruling in Mind

The Howey Test determines whether a financial product is a security. It has four key criteria, all of which must be satisfied:

- Investment of Money: There's an investment of money or assets.

- Common Enterprise: The investment is in a common enterprise.

- The expectation of Profit: There's an expectation of profit from the investment.

- Efforts of Others: The profit comes from the efforts of a promoter or third party.

Let’s apply it to Decred to see whether it's possible to have a "blockchain corporation" with stakeholders without risking a classification as a security.

Investment of Money: Decred did have a premine where 840k coins were allocated to the developers as compensation, and another 840k coins were distributed via a community airdrop. This premine isn't an investment of money per se, rather it's an initial distribution to ensure network security and community establishment. There was no institutional investment. After those initial premine, all the coins were created the same way bitcoins are created, and sold on exchanges.

Common Enterprise: Unlike many other projects, Decred doesn't have a centralized entity or company backing it. It operates as a decentralized autonomous organization (DAO). This aspect could challenge the notion of a common enterprise.

The expectation of Profit: While holders of DCR might expect the token to appreciate in value, it isn't sold or promoted with any promise of profits. The increase in token value is tied to the overall success of the platform, not to the efforts of a centralized entity or group of promoters.

Efforts of Others: With Decred's hybrid PoW/PoS mechanism, holders can participate in the network by mining or staking DCR. Profits, in the form of new DCR tokens, aren't solely derived from the efforts of others, but also from the active participation of the token holders.

Taking the XRP ruling in mind, we can add the following: a token itself may not be a security, but the method of its sale and usage could classify it as such. Also, token sales to institutional investors might be deemed securities offerings. Decred's tokens aren't sold as a traditional investment but are either mined through PoW or minted via staking. The premine was never sold to institutional investors, limiting the scope for it to be classified as a security based on the Ripple ruling.

From these analyses, it seems unlikely that Decred would be considered a security based on the Howey Test or the Ripple ruling.

Looking Ahead: A Shifting Regulatory Landscape

The Ripple Labs ruling has opened new dimensions in cryptocurrency regulation. It demonstrates that tokens themselves may not be securities, but the methods of their sale and use can potentially classify them as such. It's a precedent that brings more regulatory clarity, yet introduces new uncertainties.

The ruling represents a shift from a binary perspective of 'security' or 'non-security' towards a more nuanced understanding, reflecting the complexities inherent in cryptocurrencies. The onus is now on regulators to take this into account and provide clear guidelines for the burgeoning industry.

Again, I'm far from a legal expert. The analysis presented here is my personal understanding of a complex issue, so it's important to do your own research. One reason for posting this is to invite those more knowledgeable in this field to educate me or correct me.

And as always, hold on to your principles of censorship resistance and decentralization. It's crucial to maintain these foundational beliefs, even as we navigate through the evolving landscape of cryptocurrency regulation. This underpinning will serve as a compass, helping us to remain rooted, yet adaptable, as we shape the future of cryptocurrency.

Comments ()